Computer Age Management Services Ltd – Leading Registrar and Transfer Agent for MFs

Incorporated in 1988 and headquartered in Chennai, Computer Age Management Services Ltd (CAMS) is India’s leading and fastest-growing Qualified Registrar and Transfer Agent (QRTA) for Mutual Funds (MFs). With a market share of 68% based on average asset under management (AAUM), the company serves 10 out of 15 largest MF, including the top 4. The company also provides tech enabled financial infrastructure and services to diverse financial institutions such as asset management companies (AMC), alternative investment funds (AIFs), and insurance companies, payment & account aggregator and central record keeping agency for NPS. As of 31 December 2024, the company has a wide physical network comprising 286 service centres spread across 25 states and 5 union territories.

Products and Services

CAMS offers diverse services such as MF RTA, digital onboarding services; transaction processing, record management, fund accounting etc for AIF and PMS; insurance repository services; account aggregator for banks, NBFCs, investment advisors etc; streamlining the NPS journey of customers through eNPS registration, UPI-based bank account verification etc; KYC registration agency, RBI authorised payment aggregator, digital transformation, software solutions etc.

Subsidiaries: As of FY24, the company has 10 subsidiaries.

Investment Rationale

- Expanding market penetration – The company secured three MF-RTA mandates—Jio BlackRock MF, Pantomath MF, and Choice MF. Additionally, it marked a significant milestone by winning its first international MF-RTA mandate from CeyBank AMC. CAMSREP, the company’s wholly owned subsidiary, has entered into an agreement with Life Insurance Corporation of India (LIC) to provide insurance repository services. Furthermore, CAMS has formed a joint venture with KFin Technologies Ltd. to jointly own, develop, maintain, and operate the investment management platform and ecosystem known as ‘MF Central’ (“Transaction”). In the Alternate Investment Fund (AIF) segment, the company onboarded 21 new clients in Q3FY25. In its insurance repository business, the company secured a deal with Star Union Dai-ichi, making it the second life insurer to opt for 100% policyholder coverage with CAMS. On the insurance side, it is targeting an increase in policies under management from the current Rs.10 lakh to Rs.15 lakh per quarter.

- Strong operational performance – The company achieved its highest ever transaction volume of Rs.24 crore (56% YoY growth) during Q3FY25. AUM grew 38% to Rs.46 trillion on the back of strong equity assets growth at 51%. Unique investors grew by 31% to 3.90 crore and Rs.0.98 crore new SIP registrations were enrolled (a surge by 49% YoY), thereby increasing the SIP book to ~Rs.6 crore. Live investor folio increased by 35% during the quarter to Rs.9 crore accounts. These signify the company’s elevated revenue generation potential, strengthened market leadership and wider investor base.

- Q3FY25 – During Q3FY25, the company reported revenue of Rs.370 crore, a growth of 28% as compared to the Rs.290 crore of Q3FY24. This is backed by a 28% growth in MF revenue and 22% growth in non-MF revenue. EBITDA increased by 34% from Rs.130 crore of Q3FY24 to Rs.174 crore of the current quarter. Net profit increased from Rs.89 crore of Q3FY24 to Rs.125 crore of Q3FY25, a growth of 40% YoY. EBITDA margin improved from 45% to 47% and net profit margin increased from 31% to 34% YoY.

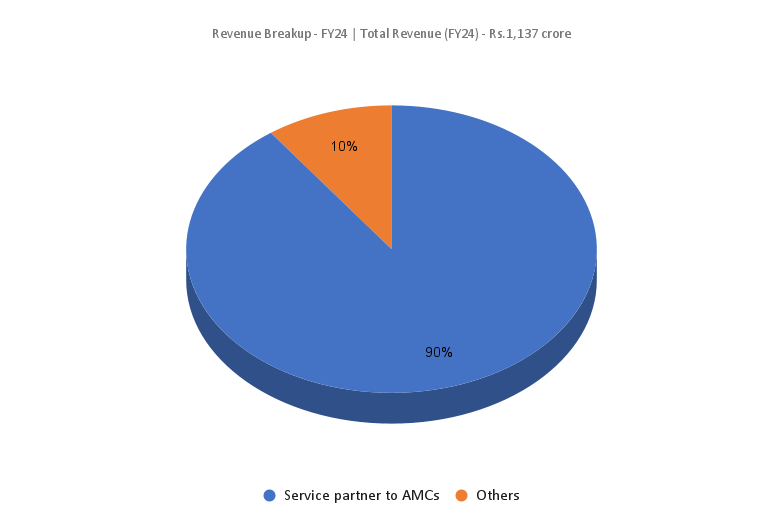

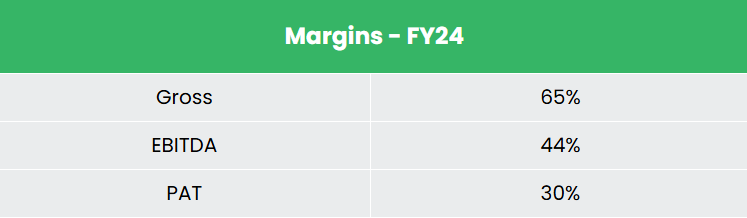

- FY24 – Rapid growth in transaction volumes and SIPs and buoyant investor confidence in capital markets has aided the company to generate a revenue of Rs.1,137 crore, an increase of 17% compared to the FY23 revenue. Operating profit is at Rs.505 crore, up by 20% YoY. The company reported net profit of Rs.354 crore, an increase of 24% YoY.

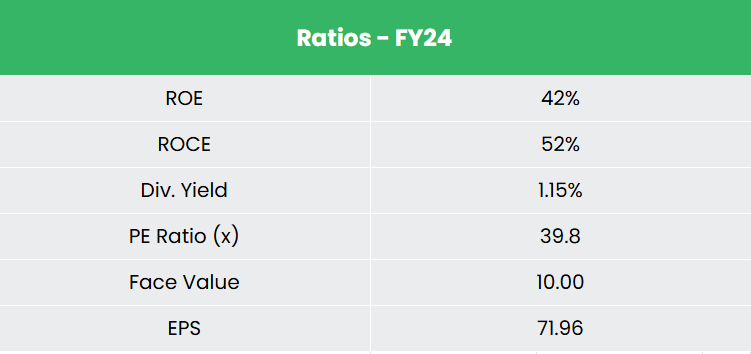

- Financial Performance – The company has generated revenue and net profit CAGR of 17% and 25% over the period of 3 years (FY21-24). Average 3-year ROE & ROCE is around 41% and 50% for FY21-24 period. The company has a debt-to-equity ratio of 0.09.

Industry

India’s financial sector – which includes commercial banks, insurance providers, non-banking financial companies (NBFCs), cooperatives, pension funds, mutual funds, and other smaller financial institutions – is witnessing rapid growth. This expansion is driven by both the robust performance of existing firms and the entry of new players into the market. With strong support from both the government and private sector, along with the fast-paced adoption of mobile and internet technologies, India is emerging as one of the world’s largest digital markets. As of FY25 (up to January 2025), the mutual fund industry’s Assets Under Management (AUM) reached Rs.68.05 lakh crore (US$ 789.44 billion). During the same period, investments through Systematic Investment Plans (SIPs) totalled Rs.2,37,427 crore (US$ 27.54 billion).

Growth Drivers

- Lower mutual fund penetration of 5-6% reflects latent growth opportunities given the rise of salaried middle-class population.

- The Union Budget 2025 has announced an increase of FDI sectoral cap for the insurance sector from 74% to 100%. This enhanced limit will be available for those companies, which invest the entire premium in India.

- The reduction in the tax burden in the 2025-26 Union Budget is expected to boost the investable amount available among the expanding middle class population.

Peer Analysis

Competitor – KFin Technologies Ltd.

Compared to its competitor, the company is generating better returns from invested capital aided by a stable growth in revenue, indicating its prudent capital allocation and revenue generating capabilities.

Outlook

With a market share of ~68% based on AAUM, 62% share in new SIP registration and 70% share of NFO collection, CAMS has marked its position as a key financial intermediary in the Indian capital market. Its cutting-edge IT platforms and mobile applications have enabled the company in providing advanced technology solutions to its customers. Notably the company is securing an increasing number of inbound contracts from both domestic and international clients.

Valuation

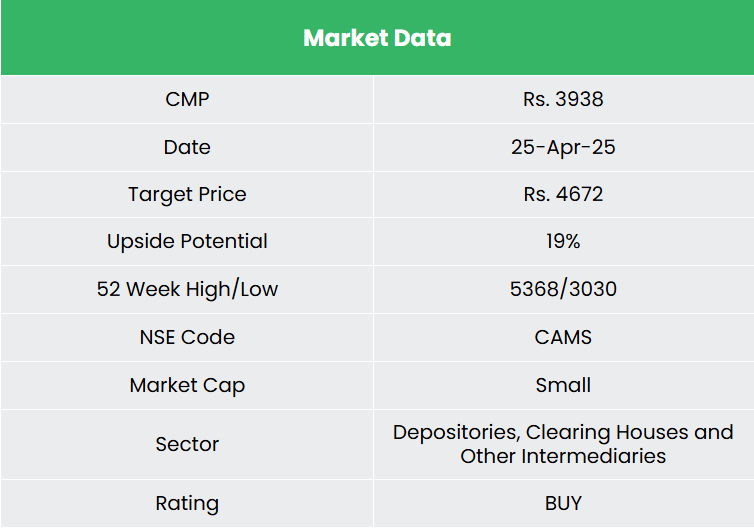

Being the market leader QRTA in India’s fast growing mutual fund industry, strongly backed by the government’s impetus on digital transformation of financial services, we believe CAMS is well positioned to accelerate its growth momentum. We recommend a BUY rating in the stock with the target price (TP) of Rs.4,672, 48x FY26E EPS.

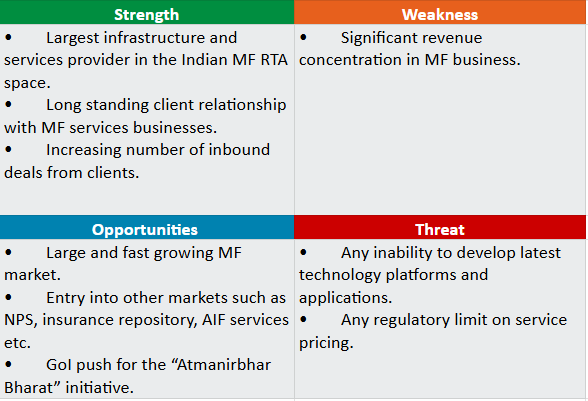

SWOT Analysis

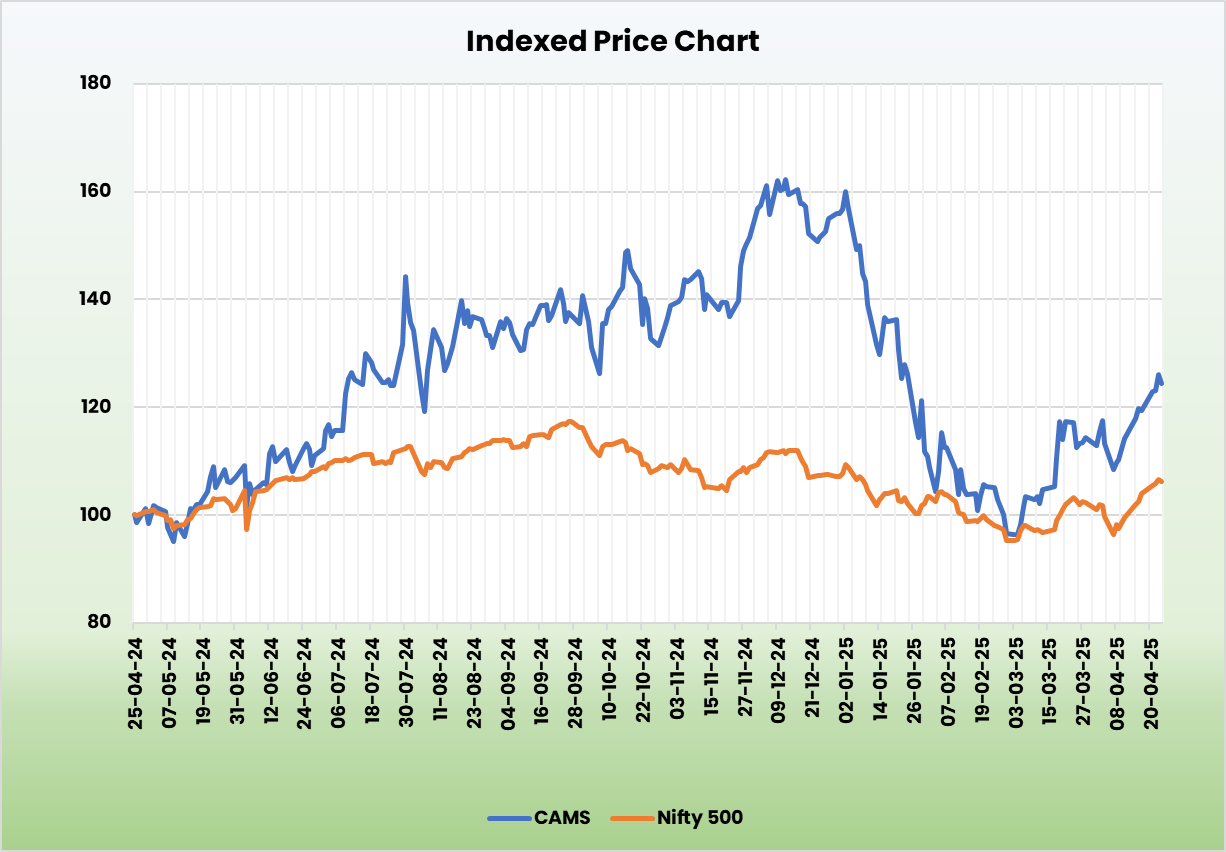

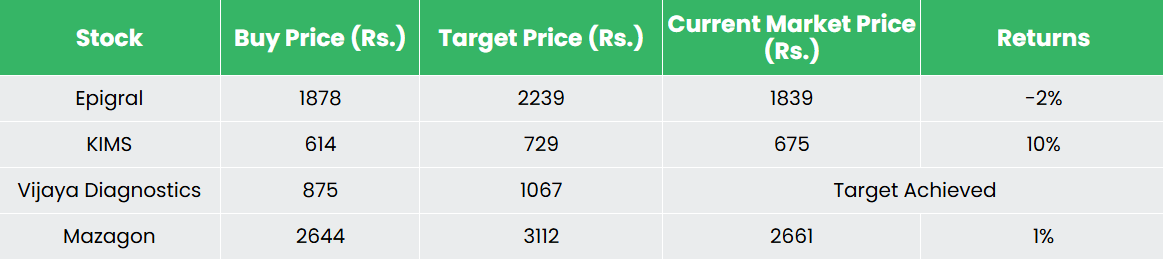

Recap of our previous recommendations (As on 25 April 2025)

Krishna Institute of Medical Sciences Ltd

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.

Other articles you may like

Post Views:

53

{kind=link}

{kind=link}