Jagbir Singh Vs ITO (ITAT Delhi)

The case of Jagbir Singh vs. ITO before the ITAT Delhi involved an appeal by the assessee challenging the legality of reassessment proceedings initiated under Sections 147 and 148 of the Income Tax Act, 1961, for the Assessment Year 2011-12. The reassessment was triggered following a report from the Investigation Wing regarding the assessee’s sale of agricultural land, which the Assessing Officer (AO) believed should have been taxed under long-term capital gains. Acting on this, the AO recorded reasons and sought approval for reopening the case under Section 151 of the Act. The assessee contested the validity of this process, particularly the approval granted by the Additional Commissioner of Income Tax (Addl. CIT), arguing that it lacked proper application of mind and failed to meet statutory requirements.

The tribunal carefully reviewed the approval memo, which formed the basis for initiating reassessment, and found significant procedural lapses. Notably, the identity of the sanctioning authority was not discernible from the record, and the approval merely stated, “Yes, I am satisfied with the reasons recorded by the AO,” without any detailed reasoning or personal analysis. This, the tribunal held, violated the purpose and procedural safeguards intended by Section 151 of the Act, which demands a reasoned and mindful evaluation by a competent authority before disturbing a concluded assessment. The tribunal referenced multiple judicial precedents, including rulings by the Delhi High Court and the Supreme Court, emphasizing that perfunctory or mechanical approvals are inadequate in law.

Given these findings, the ITAT concluded that the approval under Section 151 was invalid and, consequently, the reassessment notice and the order that followed were also void. The tribunal stressed that statutory preconditions for invoking jurisdiction under Section 147 must be strictly adhered to, and any deviation renders subsequent proceedings unsustainable. As the foundation of the reassessment—i.e., the approval—was defective, all resulting actions, including the additions made, were nullified. The tribunal therefore allowed the assessee’s appeal and set aside the reassessment order in its entirety without delving into other grounds of appeal, which were rendered academic.

FULL TEXT OF THE ORDER OF ITAT DELHI

The instant appeal has been filed at the instance of the assessee seeking to assail the First Appellate order dated 27.10.2023 passed by Ld. Commissioner of Income Tax (A), National Faceless Appeal Centre (“NFAC”), Delhi [“Ld.CIT(A)”] u/s 250 of the Income Tax Act, 1961 [“the Act”] arising from the assessment order dated 27.12.2016 passed u/s 143(3)/147 of the Act pertaining to assessment year 2011-12.

2. As per the grounds of appeal, the assessee has challenged the assumption of jurisdiction under s. 147 r.w.s 151 of the Act and also additions made by the Assessing Officer (“AO”) towards Long Term Capital gain (“LTCG”) on sale of land on merits.

3. When the matter was called for hearing, the Ld. Counsel for the assessee submitted at the outset that the assessee filed return of income for AY 2011-12 in question electronically on 07.07.2011 which was also duly processed under s. 143(1) of the Act, declaring total income of INR 12,72,890/-. Thereafter, as per the information received from the Investigation Wing of the Department, Gurgaon, the AO noted that the assessee has sold certain agricultural land parcels during the year and received consideration on sale of such land parcels.

However, the capital gains arising on sale of such land parcels are susceptible to capital gains tax as such land parcels are to be regarded as capital asset as defined under s. 2(14) of the Act.

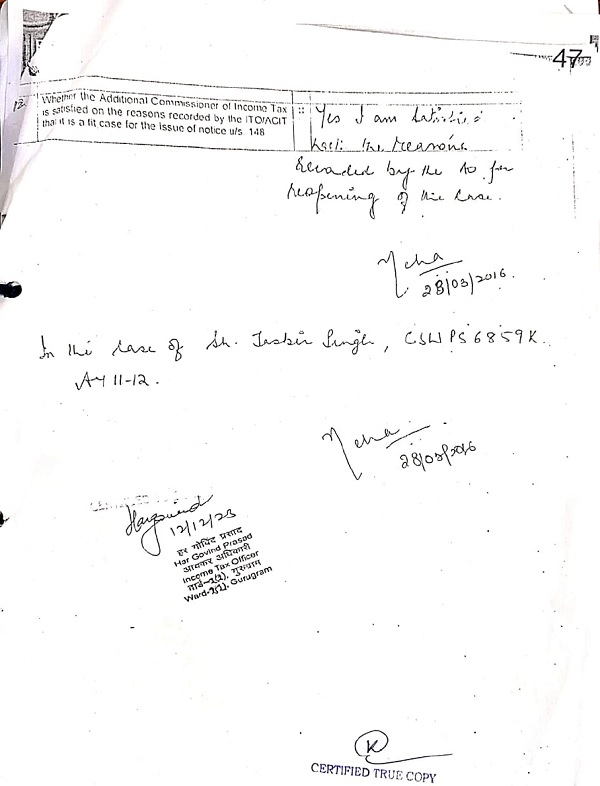

4. Based on such innocuous information without specific particulars stated to be collected by the AO alleging escapement of income in the hands of the assessee, the AO recorded reasons under s. 148(2) of the Act dated 21.03.2016 proposing of re-opening of concluded assessment in terms of section 147 of the Act by issuing notice under s. 148(1) of the Act. For the purposes of re-opening the assessment and issuance of notice under s.1 48 of the Act, the approval was sought by the AO from the Competent Authority namely, the Ld. Addl. Commissioner of Income Tax (Ld. Addl.CIT) in terms of section 151 of the Act. The approval as per requisition memo was accorded by the purported Ld. Addl.CIT on 28.03.2016. Based on such approval under s. 151 of the Act, a notice dated 28.03.2016 was issued under s. 148 for AY 2011-12 and served upon the assessee with a view to assess the alleged escapement of chargeable income.

4.1. The Ld. Counsel for the assessee at this stage, challenged the legality of assumption of jurisdiction under s. 147 r.w.s. 148 of the Act. The Ld. Counsel for the assessee submitted that the AO did not meet the pre-requisites of s. 147 of the Act and thus, the proceedings initiated under s. 147 is without jurisdiction and thus a nullity. The Ld. Counsel, in the same breath, also pointed out that the requirement of s. 151 of the Act has also not been satisfied in the instant case while recording concurrence with the so-called reasons forwarded to the Ld. Addl. CIT by the Ld.AO for sanction under s. 151 of the Act. The Ld. Counsel for the assessee exhorted that powers vested under s. 147 are inter-alia contingent upon proper sanction of the Competent Authority under s. 151 of the Act and in the absence of proper sanction, the issuance of notice under s. 148 stands vitiated and rendered nonest in law.

4.2. The Ld. Counsel for the assessee alleged that the act of sanction by the Ld. Addl. CIT is a mere tokenism and a mechanical action. Besides, even the identity and whereabouts of the sanctioning authority is not discernible in the approval memo. Furthermore, apart from obscure identity of the signatory as a sanctioning authority, the approval granted is clearly plagued with non-application of mind. The Ld. Counsel for the assessee pointed out that the Ld. Addl.CIT concerned as per Row No.12 of the requisition memo summarily states that “Yes, I am satisfied with the reasons recorded by the AO for re-opening of the case”

4.3. Delineating further, the Ld. Counsel for the assessee vociferously asserted that the purported unidentifiable Ld. Addl.CIT while granting approval has adopted a completely nonchalant approach as can be envisaged from Row No.8 of the requisition for approval where the AO had stated that no return has been filed. The AO, on the other hand, in the reasons recorded himself observed that the assessee has not disclosed capital gains in his return of income meaning thereby that ROI was actually filed. The Ld. Counsel for the assessee alleged that the purported Ld. Addl. CIT (identity, designation not known) apparently acted as a rubber stamp of the action of AO to re-open and disturb the concluded assessment based on wrong facts. The law mandates that the sanctioning authority is under statutory duty to look into the factual aspects and offer some comment in brief to justify his sanction to re-open the case in such circumstances. In the absence of any indication in the ‘satisfaction note’ by the purported Ld. Addl.CIT giving inference of application of mind, the so-called sanction under s. 151 of the Act is without any foundation.

4.4. The Ld. Counsel for the assessee adverted to the sanction so accorded by the purported Ld. Addl. CIT and submitted that a generic and cosmetic approval “Yes, I am satisfied with the reasons recorded by the AO for re-opening of the case” do not satisfy the requirement of law. Such expressions apparently smacks of a colourless and listless sanction, devoid of iota of reflection towards application of mind, if any. The Ld. Counsel for the assessee pointed out that various Courts and Tribunals have repeatedly frowned upon such sterile approval in the context of s.151 and quashed the re-assessment notice on the grounds of non-application of mind by the sanctioning authority by holding such perfunctory approval as nonest in the eyes of law.

4.5. The Ld. counsel submitted that the jurisdictional High Court as well as the Hon’ble Courts of different jurisdictions have echoed in chorus that simply noting down the expressions such as ‘Yes’ or ‘action under section 148 approved’ etc. against the column of sanction without application of mind being discernible, cannot be considered to be a proper and valid sanction by the Competent Authority. The Ld. counsel referred to judgments rendered in the case of PCIT vs. N.C. Cables Ltd., 391 ITR 11 (Delhi); Pr.CIT vs. Pioneer Town Planners Pvt. Ltd., ITA No.91/2019 judgment dated 20.02.2014 (Delhi High Court); CIT Jabalpur vs. M/s. S. Goyanka Lime and Chemicals Ltd., ITA No.82 of 2012 judgment dated 14.01.2014 (M.P. High Court) (SLP by the Revenue dismissed in CIT vs. S. Goyanka Lime and Chemicals Lid.. (2023) 453 ITR 242 (SC); Manujendra Shah vs. CIT, WP(C) 12677/2018 judgment dated 18.07.2023 and plethora of Co- ordinate Bench judgments to contend that the Competent Authority while discharging statutory obligation under s. 151 of the Act is not expected to function mechanically and accord sanction on dotted lines. The satisfaction of the Competent Authority must be recorded with some degree of objectivity based on some objective material. The Ld. Counsel for the assessee thus submitted that on this ground alone, the issuance of notice under s. 148 based on a cryptic sanction is vitiated and consequently, the assessment order framed as a sequel thereto, is rendered bad in law.

5. The Ld. Sr. DR for the Revenue, on the other hand, supported the action of the Revenue Authorities and contended that jurisdiction under s. 147 has been assumed on the basis of valid and proper sanction of the Competent Authority under s. 151 of the Act. The Ld. DR contended that the approval of Ld. Pr. CIT under s. 151 are administrative in nature and there is no requirement in law that Competent Authority needs to record its own reasons for sanction under Section 151 of the Act. Once the approval is granted, the statutory presumption is to be drawn that the Competent Authority has acted in good faith with due application of mind. The Ld. DR thus submitted that the sanction granted by the Ld. Pr.CIT cannot be faulted in law having regard to the plain language of the provisions of s. 151 of the Act.

6. We have carefully weighed the rival contentions on the preliminary challenge to the assumption of jurisdiction under s. 147 of the Act and perused the material available on record.

6.1. While several facets challenging the assumption of jurisdiction under s.147 are involved, to begin with, we consider it expedient to address ourselves on the legitimacy of approval stated to have been granted by the Ld. Addl.CIT under s. 151 of the Act as vehemently questioned on behalf of the assessee.

6.2. Since the primary issue hinges around the validity of approval of the Competent Authority to the reasons for re-opening he concluded assessment, the scanned copy of such approval memo/requisition memo under s. 151 of the Act is reproduced hereunder for easy reference:-

6.3. The reasons for re–opening the case under s. 147 of the Act are reproduced as under for ready–reference:–

6.4. A bare glance of approval memo would suggest that the AO has proceeded to initiate the action under s. 147 of the Act on the basis of so-called satisfaction of some Addl. CIT towards escapement as forwarded to him by the AO in terms of s.151 of the Act. In another words, the purported approval of the Ld. Addl. CIT under s. 151 of the Act in the instant case has galvanized the proceedings under s. 147 of the Act into motion. As the law envisage, prior permission of superior authority as statutorily designated, is a sine qua non for initiation of action under s. 147/148 of the Act. The Addl. CIT, in the instant case, is stated to be a Competent Authority statutorily designated for this purpose. It was thus, on the basis of satisfaction and approval of the Addl. CIT that the proceedings for reassessment was initiated and culminated in re-assessment order under challenge. The legitimacy of satisfaction of the purported Addl.CIT for the purposes of sanction under s. 151 has however, been called into question in the instant case.

7. As self-evident from the approval memo, the Addl. CIT who claimed to be satisfied on the reasons recorded is unidentifiable. A signature has been put granting approval but without writing the name, designation etc. of the authority who claims to be a Competent Authority for the purposes of s. 151 of the Act. In the approval memo, no indication towards whereabouts of the Competent Authority is discernible. The approval memo without the identity of the authority concerned itself vitiates the approval giving rise to the re-assessment proceedings. Such approval without the particulars of the sanctioning authority bears no sanctity in the eyes of law and vitiates the consequential actions based on such non-actionable sanction.

7.1. Furthermore, as pointed out on behalf of the assessee, the purported Addl. CIT has simply recorded “Yes, I am satisfied with the reasons recorded by the AO for re-opening of the case”. Ostensibly the sanction granted is muted and non-descript. Section 151 of the Act operates as one of the potent safeguards against any arbitrary and disproportionate exercise of powers under s. 147 by the AO. The powers conferred under s. 151 are coupled with statutory duty. It ensures that powers vested under s. 147 are not exercised by the AO unless the designated superior Officer is satisfied that the condition precedent for exercise of powers as provided erstwhile s. 147 of the Act are fulfilled. As a corollary, to meet this avowed objective enshrined in enactment of s. 151 of the Act, it is incumbent upon the superior Authority to apply its mind innately to the material available for alleged escapement and express his satisfaction on the reasons recorded.

7.2. Significantly, erstwhile s.151 of the Act is silent on opportunity to the assessee before sanctioned. The absence of any formal opportunity to the assessee rationally calls for greater degree of circumspection and restraint while evaluating the proposed action of the AO. The sanctioning authority while exercising power under s. 151 of the Act is thus expected to examine the reasons, material or grounds available and to judge whether they are relevant to formation of necessary belief on the part of the AO and thereafter, to record necessary satisfaction which should not be mechanical but as a result of application of mind as held in Chhugamal Rajpal vs S.P.Chaliha & Ors. (1971) 79 ITR 603(SC).

8. In the peculiar facts of the instant case, the purported sanction of the Addl.CIT is based on the premise that the assessee has not filed return of income at all and engaged in land deals of substantial amount. Driven by such grossly incorrect factual position, the Addl.CIT has granted sanction resulting in civil consequences to the assessee.

8.1. This apart, an omnibus approval without any comment on any aspect betrays the application of mind on foundational points recorded in reasons for reopening. The approval granted do not utter a word towards any reasons which induced him to obtain satisfaction on the alleged escapement claimed by the AO.

8.2. Under these circumstances, we compelled to think that approval under s. 151 grossly suffers from the vice of non-application of mind. The Hon’ble Delhi High Court in the case of N.C. Cables; Pioneer Town Planners; Manujendra Shah (supra) have struck a balance and declined to endorse a rubber stamp approval granted by the Competent Authority under s. 151 of the Act.

9. In the light of delineations made, we see palpable merit in the plea of the assessee that the sanction granted under s. 151 of the Act is extraneous and an empty formality and do not accord with its salutary purpose. Notwithstanding, in the absence of identity of the person on record who granted sanction under s. 151 of the Act, such so-called sanction is a dead document devoid of any semblance in the eyes of law. Needless to say, the validity of re-assessment order is contingent upon the valid approval under s. 151 of the Act. Where the identity of sanctioning authority itself is under cloud and coupled with this, the requirement of law to grant speaking approval under s. 151 of the Act is not found to be fulfilled, the notice issued under s. 148 as a sequel to such sanction and resultant assessment would also to be vitiated in law.

10. We are thus disposed to hold that the re-assessment proceedings under s. 147 as a consequence of nonest and invalid approval is without sanction of law and consequently, the re-assessment order in question is bad in law. Hence, the jurisdiction usurped by the AO based on such approval is required to be cancelled and set aside. This being so, the other aspects touching the jurisdiction and other grounds raised in the memo of appeal are rendered academic and hence not adjudicated. The additions made in a nonest reassessment order thus merges in void.

11. In the result, the appeal of the assessee is allowed.

Order pronounced in the open Court on 08th January, 2025.

{kind=link}