Cummins India Ltd – Power, Progress, Possibilities.

Founded in 1962 and headquartered in Pune, Cummins India Ltd. is a leading manufacturer of diesel and natural gas engines in the country. The company specializes in designing, producing, distributing, and servicing engines and related technologies, including fuel systems, air handling, filtration, emission solutions, and electrical power generation systems (gensets). As of FY24, the company operates 5 factories, 1 parts distribution centre, 480+ service touchpoints and 120 retail touchpoints serving industries such as construction, compressor, mining, marine, railway, oil and gas, pumps, defence and power generation. With a broad global presence, the company serves markets including Nepal, Bhutan, the USA, Europe, Mexico, Africa, the Middle East, and China as its key destinations.

Products and Services

The company’s products are categorised across 4 business segments:

- Engine Business – Manufactures engines from 60 HP for on-highway commercial vehicles and off-highway commercial equipment industry spanning construction and compressor.

- Power Systems Business – Manufactures high horsepower engines for marine, railways, defence and mining applications as well as power generation systems comprising of integrated generator sets.

- Components business – Consists of 4 businesses such as Filtration, Turbo Technologies, Emission Solutions and Electronics and Fuel Systems.

- Distribution business – Provides products, packages, services and solutions for uptime of equipments.

Subsidiaries: As of FY24, the company has 1 subsidiary, 1 associate company and 1 joint venture.

Investment Rationale

- Growth strategies – The company has currently localized 70-75% of its product and is working to increase this share, which would enhance margins, pricing power, and profitability, while strengthening its market position. The company’s industrial segment has achieved strong performance driven by robust demand in construction segment and railways. While management remains cautious due to the cyclical nature of the construction industry, they are optimistic about order inflows in the railway and mining sectors. The company has also launched products in the US markets which has similar emission norms as that of India. Optimised capacity utilisation has also led to a decrease in the lead time from 60 days to 30 days. The company is also advancing its HELM Technology (High Efficiency, Lower Emissions, Multi-fuel technology), which will allow engines to run on a variety of fuels, including propane, biogas, and hydrogen, among others. It is also focusing on expanding its reconditioning and distribution business.

- Market leader – In FY24, the Central Pollution Control Board (CPCB) introduced the latest and most stringent standards for diesel generators in India, replacing the CPCB II norms with the CPCB IV+ regulations. These new CPCB IV+ norms are expected to significantly reduce harmful pollutants such as NOx, CO, HC, and PM. Cummins India was among the first companies in the country to receive regulatory approval for manufacturing CPCB IV+ compliant gensets. The company’s products have already been well received in the market, and by Q3FY25, CPCB IV+ gensets accounted for approximately 40% of total genset sales for the company. The management believes that pricing for CPCB IV+ products would take 2-3 quarters to stabilise.

- Q3FY25 – During the quarter, the company generated revenue of Rs.3,096 crore, an increase of 22% compared to the Rs.2,541 crore of Q3FY24. Exports improved by 43% while domestic sales increased by 18%. Operating profit increased from Rs.543 crore of Q3FY24 to Rs.598 crore of Q3FY25, a growth of 10%. The company reported net profit of Rs.558 crore, an increase by 12% YoY compared to Rs.499 crore of the corresponding period of the previous year.

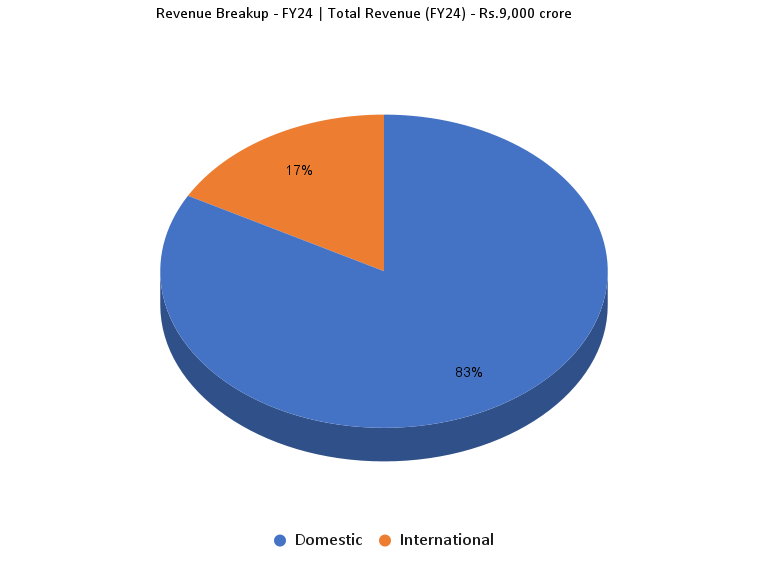

- FY24 – During the FY, the company generated revenue of Rs.9,000 crore, an increase of 16% compared to the FY23 revenue, aided by a 31% growth in domestic sales. Operating profit is at Rs.1,761 crore, up by 42% YoY. The company reported net profit of Rs.1,721 crore, an increase of 40% YoY.

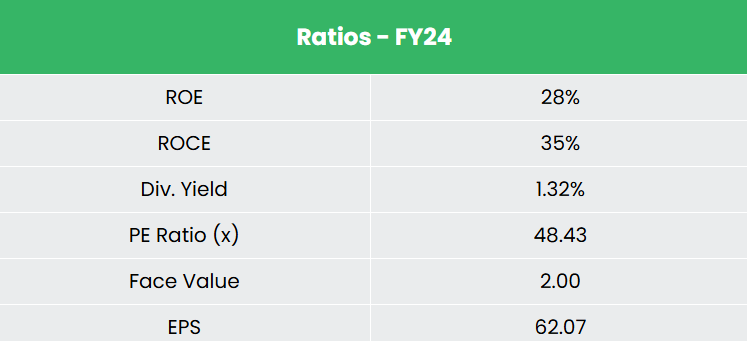

- Financial Performance – The 3-year revenue and net profit CAGR stands at 27% and 37% respectively between FY21-24. The company has strong balance sheet without any debt in its capital structure. Average 3-year ROE and ROCE is around 23% and 28% for FY21-24 period.

Industry

India’s capital goods sector is a powerful growth driver, fuelled by government investments in infrastructure and a focus on manufacturing, presenting substantial investment opportunities. The electrical equipment market in India is projected to grow from US$ 52.98 billion in 2022 to US$ 125 billion by 2027, reflecting a strong compound annual growth rate (CAGR) of 11.68%. The growth of the engineering sector is being significantly supported by various policies and initiatives from the Indian government. Incentives aimed at expanding power generation capacity will further boost the demand for electrical machinery.

Growth Drivers

- The government has de-licensed the engineering sector with 100% FDI permitted.

- The domestic demand is expected to be robust as the adoption of CPCB IV+ norms picks up.

- The ‘Make in India’ initiative, along with the government’s emphasis on improving the ease of doing business, is expected to create numerous opportunities in the engineering and capital goods sectors in the coming years.

Peer Analysis

Competitors: Kirloskar Oil Engines Ltd, Greaves Cotton Ltd, etc.

Among the above competitors, Cummins has better return ratios and stable revenue growth, indicating the company’s financial stability and its efficiency to generate income and returns from the invested capital.

Outlook

It is encouraging to note that the company has achieved consistent segmental performance YoY, with domestic genset sales increasing by 18%, the distribution business growing by 13%, industrial domestic sales rising by 24%, and exports in both HHP and LHP growing by 47%. Currently the company has a robust portfolio of CPCB-IV+ compliant products to meet the customer demand across the entire product range. Its ongoing efforts in supply chain improvements and value additions is expected to improve the market penetration. The company has successfully reversed the previous downward trend in export sales, with notable growth primarily coming from the Middle East and Latin American markets. By meeting CPCB IV+ standards, we believe the company is positioned to be a key player in the Indian power generation market, offering cleaner and more environmentally friendly diesel generators. The company has also projected double-digit sales growth for FY25.

Valuation

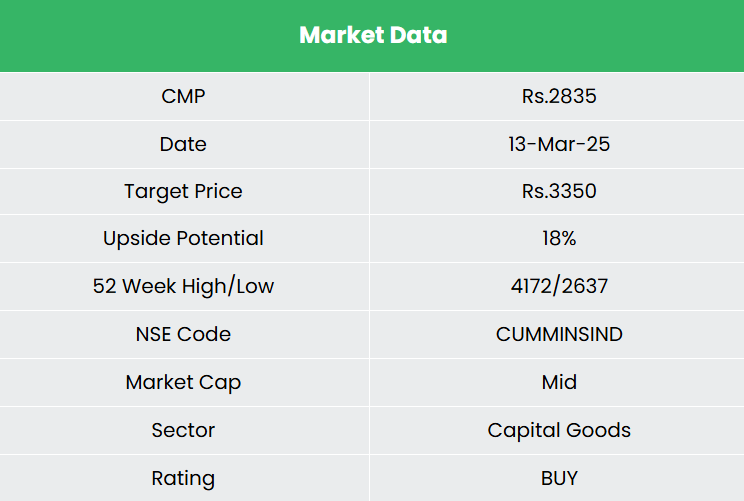

We believe the company is expected to grow in tandem with the nation’s increased infrastructure spending. We recommend a BUY rating in the stock with the target price (TP) of Rs.3,350, 31x FY26E EPS.

Risk

- Geopolitical instability – Changing policy dynamics and supply chain disruptions due to geopolitical conflicts might adversely impact the company’s operations.

- Forex Risk – The company has significant operations in foreign markets and hence is exposed to forex risk. Any unforeseen movement in the forex market can adversely affect the company.

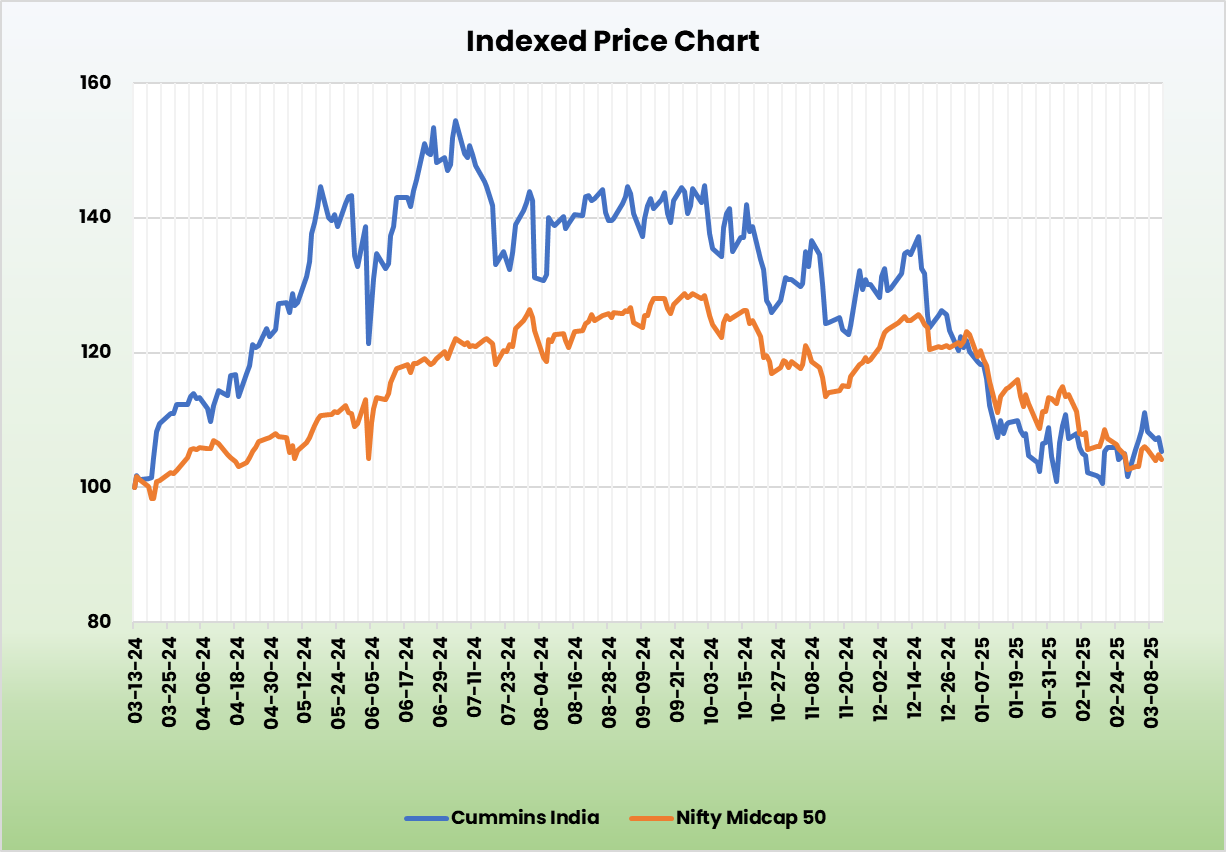

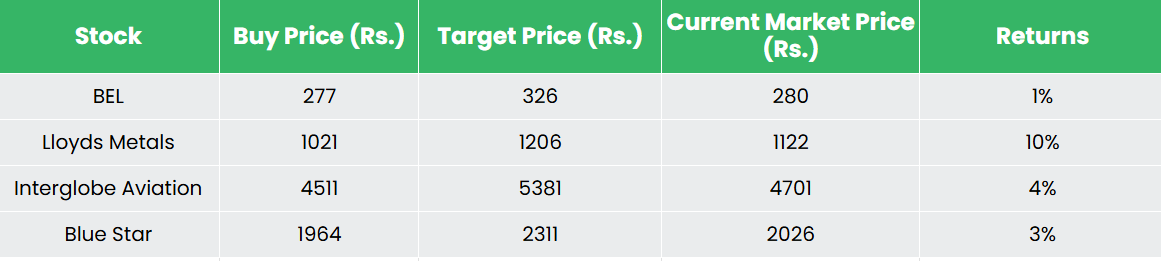

Recap of our previous recommendations (As on 13 March 2025)

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.

Other articles you may like

Post Views:

78

{kind=link}

{kind=link}